Article content

An adult child calling about rent, a car repair, or a bill they can't cover puts you in a hard spot fast. You want to help. You also have a fixed income that was never built to absorb someone else's emergency.

Retirement-income researchers are starting to flag this exact pressure: parents quietly draining savings and future security to bail out grown kids, one loan at a time. Before you say yes to anything, run your own numbers. Then decide, on purpose, what kind of help fits.

Choose your next move

Decide the kind of help you're open to right now

Pick the option that matches where you actually stand today, not where you wish you stood.

A set dollar amount, a one-time gift, or a short-term loan with terms — not an open-ended commitment.

Run Your Numbers Before You Say Yes

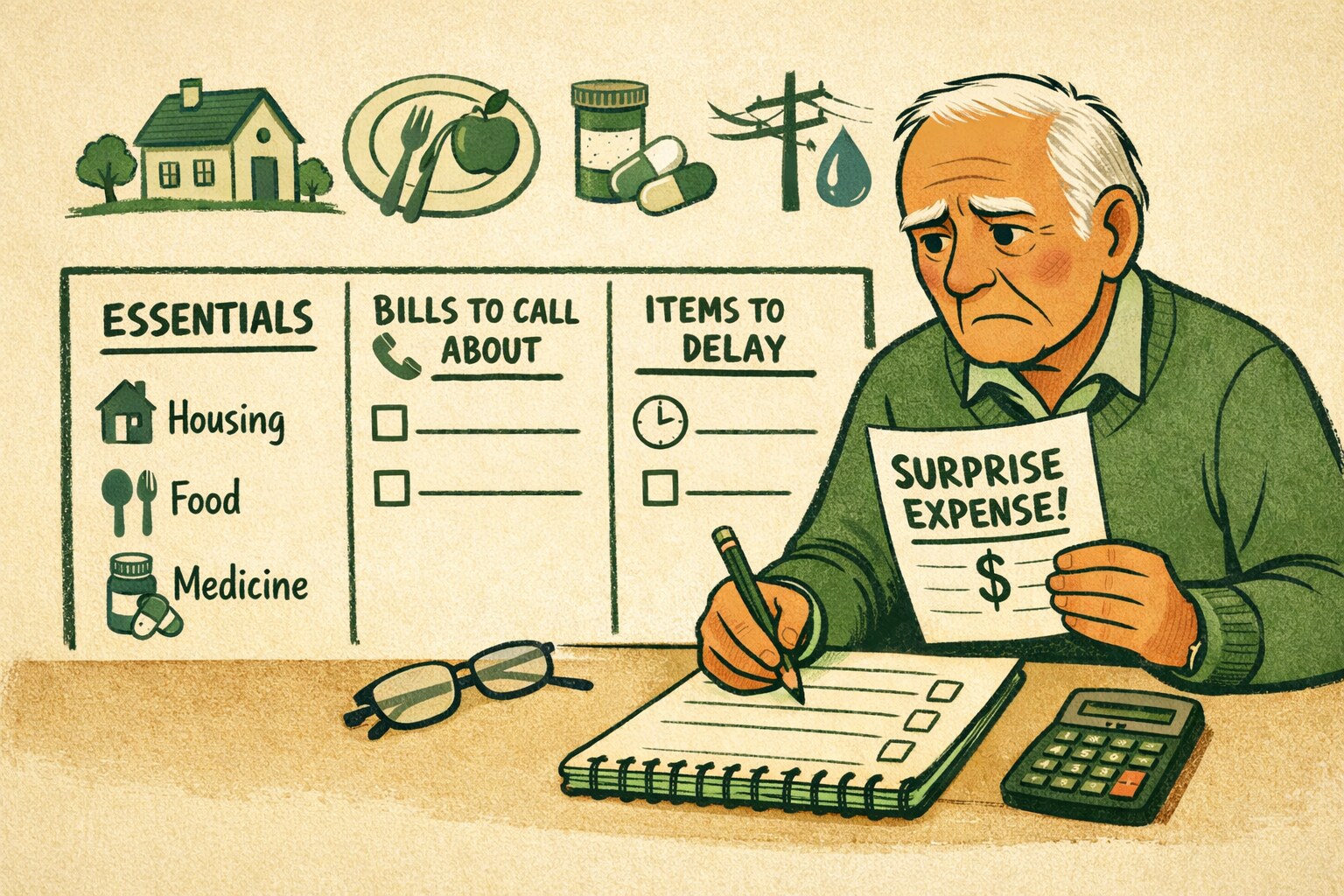

Guilt moves fast. Math moves slower, and it's the only thing that should decide this. Before you offer a dollar figure, know exactly what's left after your own housing, food, medications, and utilities are covered.

This isn't about loving your child less. It's about making sure a loan you can't really afford doesn't turn into your own emergency six months from now.

Quick calculator

Check what's left after your own essentials

Enter your real numbers before you name a figure to your child.

Essential spending total: $2,030

Cash left after essentials: $970 • Essentials use 68% of income.

If this number is small or negative, the honest answer is limited help or no money help at all — and that's a legitimate answer.

Decide What Kind of Help Actually Fits

Once you know your number, decide the shape of the help, not just the amount. A one-time gift, a loan with a written payback date, or covering one specific bill directly are all different commitments — pick one on purpose instead of drifting into whatever your child asks for.

If {{budgetCheck.result|currency}} is tight, a {{helpStance.label|defined amount}} protects you both: your child gets clarity, and you don't quietly become their backup budget every month.

Checklist

Set these terms before any money moves

A short conversation now prevents a longer one later.

0 of 4 done.

If this request landed on top of a bill of your own, read Handling a Sudden Expense Without Panic before you commit anything.

Say It Out Loud Without Guilt

The hardest part usually isn't the math — it's the sentence. Practice saying the number and the terms before your child is on the phone waiting for an answer. A calm, specific answer holds up better than a rushed yes you'll regret.

Timeline

Work the conversation in order

Check off each step as you go.

Confirm $970 left after essentials before you say a dollar amount out loud.

Write the amount, the terms, and one thing you won't cover again.

State the I can help, but only in a defined way plainly, then stop talking and let your child respond.

Save your plan

Save your numbers and terms so you don't have to reconstruct them under pressure next time.

Common questions

How do I decide how much money to give my adult child?

Run your numbers first — know exactly what's left after your own housing, food, medications, and utilities are covered before you offer a dollar figure. If what's left is small or negative, limited help or no money help at all is a legitimate answer.

Should I give my adult child a gift or a loan?

Decide the shape of the help on purpose, not just the amount. A one-time gift, a loan with a written payback date, or covering one specific bill directly are all different commitments — write down which one you're offering and, if it's a loan, agree on a repayment date in writing.

What should I ask my adult child before giving them money?

Ask what they've already tried — a payment plan, a hardship program, or a side gig — before you become the plan. It's also worth pointing them to Benefits.gov to check what public assistance they may already qualify for.

How do I set limits with my adult child without feeling guilty?

Practice saying the number and the terms before your child is on the phone waiting for an answer, and name what you won't cover again without a new conversation. A calm, specific answer holds up better than a rushed yes you'll regret.