Article content

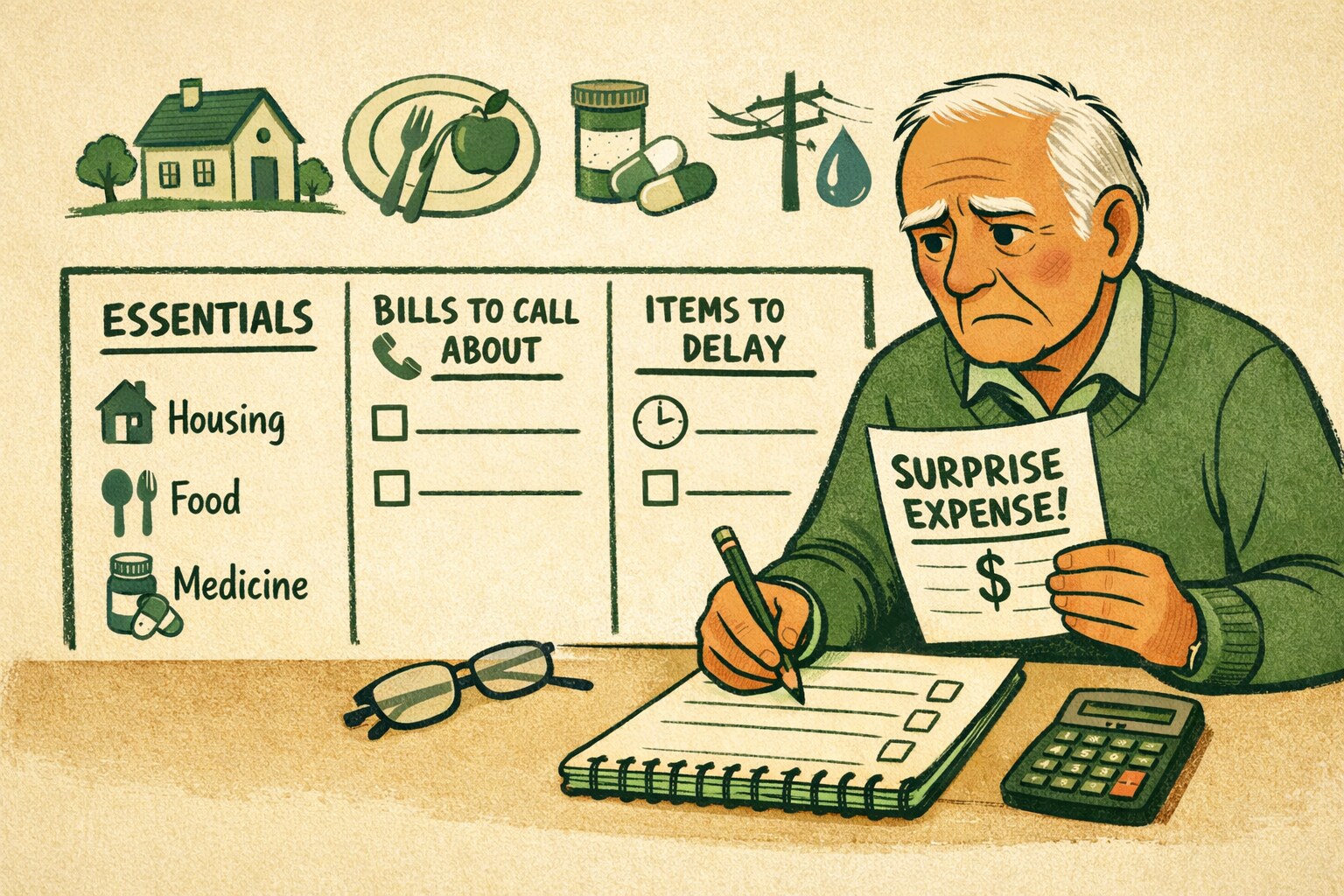

Start by listing every bill due in the next 30 days, then mark housing, food, medications, and utilities as the expenses you protect first. That order gives the rest of the decisions some discipline.

Once you know what must stay current, call the new bill issuer within two business days and ask about hardship terms before any payment is missed.

While that new expense is being sorted out, pause optional subscriptions and auto-renewals for one month so cash stops leaking in the background.

Write down each call with the date, the representative's name, and the payment terms offered. Those notes make it much easier to compare options and catch bad follow-through.

Then use a one-page weekly budget check-in for the next month so one emergency bill does not quietly turn into several late fees.

Common questions

What's the first thing I should do when a surprise bill shows up?

List every bill due in the next 30 days, then mark housing, food, medications, and utilities as the ones you protect first. That order gives you a clear starting point instead of guessing which bill to handle first.

How fast should I contact a company about a bill I can't pay?

Call within two business days and ask about hardship terms before you miss a payment. Waiting until after a missed payment gives the company less reason to work with you.

How do I stop one sudden bill from turning into several late fees?

Pause optional subscriptions and auto-renewals for a month so cash stops leaking in the background, and run a one-page weekly budget check-in for the next month. That keeps one emergency bill from quietly spreading into a bigger problem.

What should I write down when I call about a bill?

Note the date of the call, the representative's name, and the exact payment terms offered. Those details make it easy to compare offers later and catch anyone who doesn't follow through.