Article content

Half of retirees will need some kind of long-term care after they turn 85, according to a recent breakdown of retirement-planning gaps. That could mean a few months of in-home help after a hospital stay, or years in an assisted living community. Most monthly budgets don't have a line for either one.

You don't have to solve the whole problem today. Start by finding out how much room your budget actually has, then build the habit of protecting that room before a bill forces the question.

Choose your next move

Pick the scenario closest to yours

Choose the one that would hit your budget hardest if it happened this year.

Recovery care, a home health aide, or help after a fall or surgery.

What 'Half of Retirees' Actually Means for Your Numbers

That 50% figure isn't a scare statistic. It's a planning fact, the same way knowing your roof has a 20-year lifespan is a planning fact. It doesn't tell you when care starts or how long it lasts, only that betting your budget will never need to stretch for it is a bad bet for half of retirees.

The real question isn't whether to worry. It's whether your monthly numbers have room to absorb a new cost without your housing, food, or medications getting squeezed first.

Checklist

Check these before you build a plan

A clear-eyed starting point beats a guess.

0 of 3 done.

Build the Cushion Before You Need It

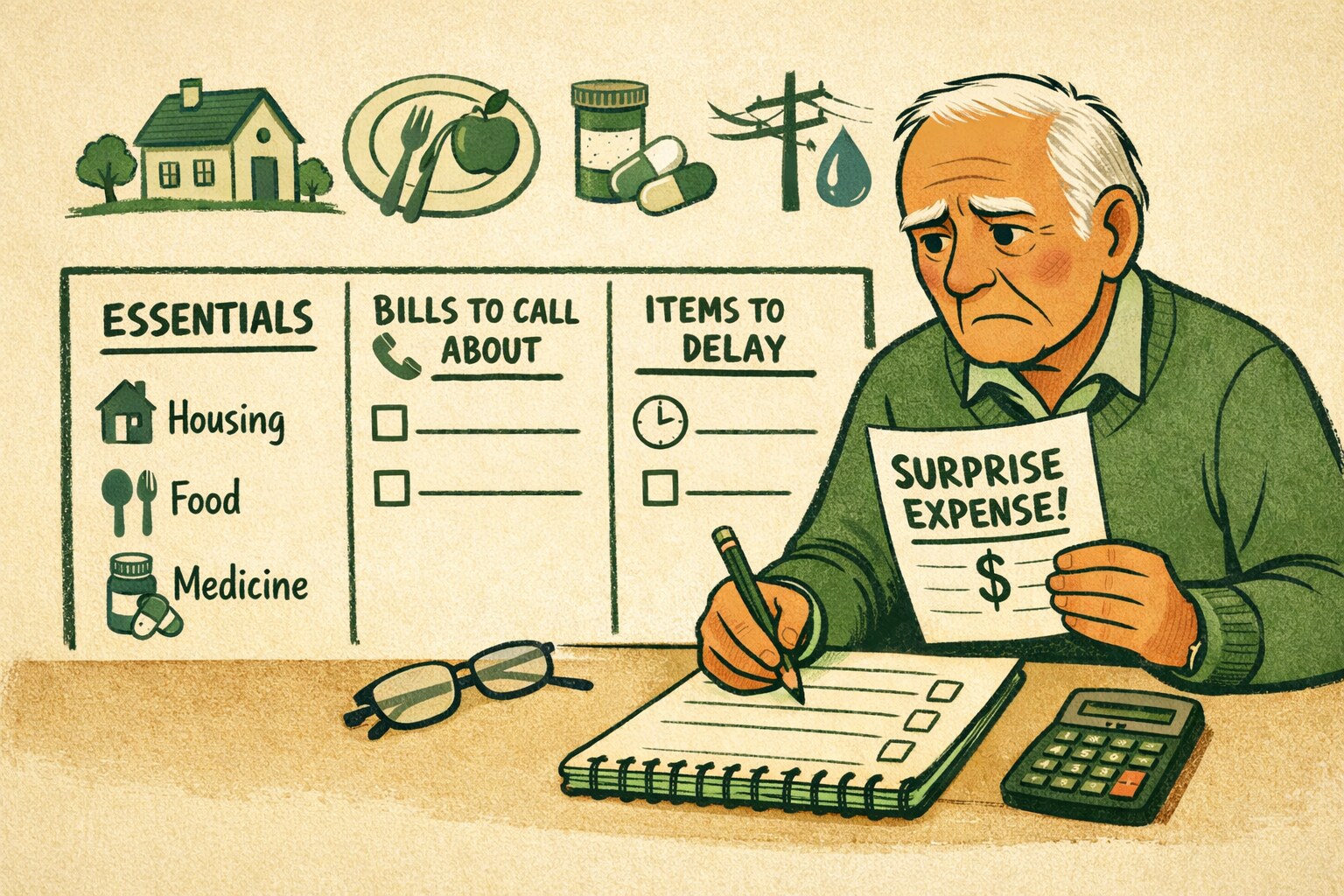

A care cushion works the same way an emergency fund does: it's cash that exists specifically so a new cost doesn't force you to cut something essential. The number that matters isn't your total savings. It's how much room is left every month after the basics are covered.

Quick calculator

Find your monthly cushion

Enter your monthly income and essential costs to see what's left over for A few months of in-home help.

Essential spending total: $2,230

Monthly cushion: $970 • Essentials use 70% of income.

If this number is thin, redirecting even a small amount toward a dedicated care fund each month is worth starting now, before A few months of in-home help arrives.

If a Bill Arrives Before the Plan Does

Plans are worth building, but bills don't always wait for you to finish one. If a care cost lands this month and your cushion isn't there yet, the order still matters: protect essentials first, then negotiate the new bill instead of paying it in full on reflex.

Checklist

Do these before you pay a care bill in full

A short pause here protects the rest of your budget.

0 of 3 done.

If a sudden bill hits before you've read this whole plan, Handling a Sudden Expense Without Panic walks through the first 72 hours in more detail.

Know Which Programs Might Help

Medicare covers short-term, medically necessary care after a qualifying hospital stay, not an open-ended stay in assisted living. Medicaid covers long-term care for people who meet income and asset limits, which vary by state. Knowing which bucket a cost falls into now saves a confused phone call later.

Timeline

Check your options in order

Work through these before you assume a cost is entirely out of pocket.

Confirm whether your situation qualifies as short-term, medically necessary care under Medicare's rules.

Income and asset limits vary widely, so check your state's specific rules rather than a national average.

Update your $970 cushion as income, costs, or care needs change.

If you're weighing a move to a continuing care community as part of this plan, What a CCRC Contract Really Locks You Into Before Signing is worth reading before you sign anything.

Save your plan

Save your numbers and next steps so the plan is ready before you need it.

Common questions

How likely am I to need long-term care in retirement?

About half of retirees will need some form of long-term care after age 85, whether that's a few months of in-home help or a longer stay in an assisted living or nursing facility. It's a planning fact, not a prediction of what will happen to you specifically — the useful move is making sure your monthly budget has room to absorb a new cost if it comes.

Does Medicare pay for long-term care?

Medicare covers short-term, medically necessary care after a qualifying hospital stay, not an open-ended stay in assisted living or a nursing home. For longer-term care, Medicaid is the program that typically applies, and it comes with income and asset limits that vary by state.

What should I do if a care bill arrives before I've built a cushion?

Protect essentials first — housing, food, medications, and utilities — then negotiate the new bill instead of paying it in full right away. Ask the provider about a sliding scale, hardship discount, or payment plan, and confirm whether Medicare, Medicaid, or a supplemental policy covers any part of the cost before you send money.

How much should I set aside for long-term care?

Start with your monthly cushion — what's left over after essentials — rather than a single savings target. If that cushion is thin, redirecting even a small amount toward a dedicated care fund each month is worth starting now, before a need arrives, and revisiting the number every few months as your situation changes.