Article content

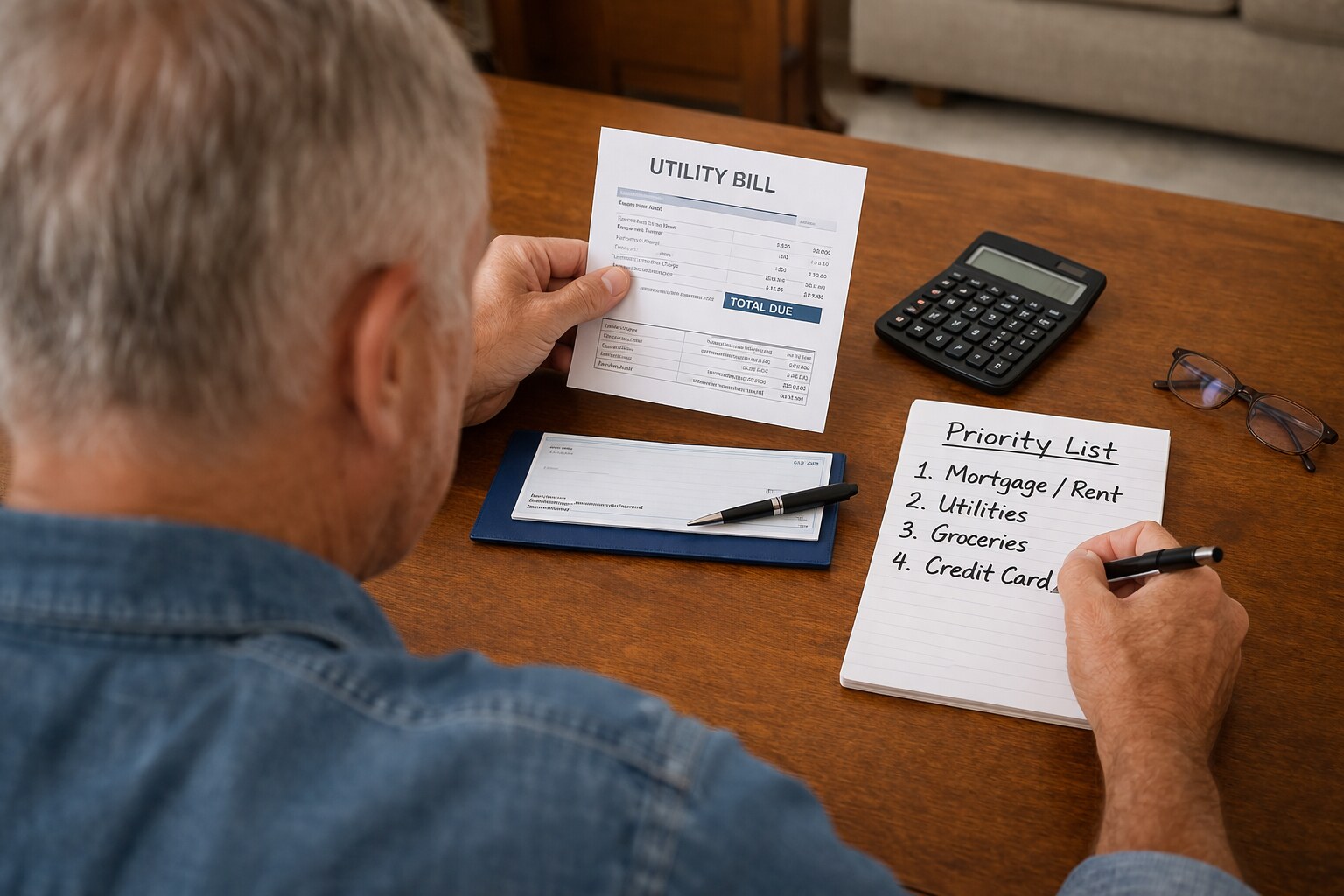

When a major bill lands, protect the basics first: housing, medication, utilities, food, and insurance. Everything else can wait until you know those essentials are covered.

Personalize this article

Name the bill so the plan feels concrete

This stays in your browser and will be used to personalize the rest of the article.

Personalize this article

Who needs payment or a phone call?

If you know the office name now, add it here so your notes and download are ready.

With that order in mind, make a one-page snapshot of income, fixed bills, and available cash. It gives you a steadier baseline before you start making cuts or promising payments.

Quick calculator

Protect essentials before you promise new money

Run the numbers for this month before you commit to .

Essential spending total: $2,230

Cash left after essentials: $970 • Essentials use 70% of income.

If this result is negative, your first job is to protect the basics and ask for relief on instead of guessing.

Next, call providers before the due date and ask about hardship options, interest pauses, or extended payment plans. Early calls usually produce better options than late apologies.

Choose your next move

Choose the first move that fits your numbers

With $970 left after essentials, pick the path that best protects this week.

Use this when $970 is tight or negative. Your script should focus on avoiding penalties while protecting housing, food, utilities, and medications.

Keep the script short: I can pay something now, but not the full amount. What hardship or installment options can we set up today to avoid penalties?

Checklist

Do these before the week gets noisy

These are the moves that keep from becoming two problems.

0 of 4 done.

If taxes are part of the problem, keep the federal filing deadline in view and ask about payment arrangements as soon as possible. Missing the deadline creates a second problem you do not need.

While cash is tight, pause non-essential subscriptions for one month. Small recurring charges are easy to ignore until they start stealing money from the categories that actually matter.

Try not to use high-interest debt for routine bills unless it prevents a critical shutoff. If you do need credit, pair it with a clear payoff timeline immediately so the emergency does not become a habit.

Timeline

Seven-day follow-up calendar

Check off each step as you go and leave yourself a note when you get a confirmation number or deadline.

Write down the amount for , the due date, and the name or number for .

Use your Ask for hardship help first approach and ask what can be set up right now.

Review housing, food, medications, and utilities again after the call.

Confirm you received the promised letter, email, portal note, or new due date.

Save your plan

Save the personalized plan from this article before you move on to the next call.

Then put everything on a seven-day follow-up calendar: who you called, what was promised, and what confirmation is still missing. Good notes are what keep a rough week from turning into a messy month.

Common questions

What should I pay first if I suddenly can't afford all my bills?

Protect housing, medication, utilities, food, and insurance before anything else — those are the essentials that keep a rough week from turning into a crisis. Build a one-page snapshot of your income and fixed bills next, so you know exactly how much cash is left before you promise money to the new bill.

What do I say when I call a company about a bill I can't pay in full?

Keep it short: tell them you can pay something now, but not the full amount, and ask what hardship or installment options they can set up today to avoid penalties. Call before the due date, not after — early calls get better options than late apologies. Have the balance, due date, and account number written down before you dial, and ask for written confirmation of whatever they agree to.

Should I put a sudden bill on a credit card if I'm short on cash?

Only if the alternative is a critical shutoff, like losing power or water. High-interest debt turns one emergency into a longer one. If you do use credit, set a clear payoff timeline right away instead of letting the balance sit.

How do I keep a bill negotiation from falling through after I hang up the phone?

Follow a seven-day calendar. Record the facts the day the bill arrives, make your first call within 24 hours, confirm housing, food, medications, and utilities are still covered within three days, and by day seven check that you actually received the promised letter, email, or portal note. No paperwork means the deal isn't real yet.